If you love your dog like I adore mine, then you may be interested in learning how to save on your vet bills. I'd pay almost any amount of money to make sure that my JRT, Cody, is safe, healthy and comfortable in life, but sometimes the sting of the vet bill has made me wish I had invested in pet insurance!

There are three easy steps you can take to not only ensure your pet stays healthy but to also save you money at the vet.

3 easy rules to abide by

1. Don't fee your dog like he's a human. Even if you're a very healthy eater by human standards, you shouldn't feed your dog human food. Their tummies cannot digest the same food and ingredients that human tummies can. You can avoid an unnecessary trip to the vet and the racking up of your vet bills by feeding your dog food for dogs!

Especially avoid:

1. Bones (or foods with bones in them such as turkey and chicken)

2. Cheese

3. Chips

4. Chocolate

5. Grapes and raisins

2. Exercise your pet to keep them at a normal weight. Make sure that you feed your pet the proper amount of food and that they get exercise on a daily basis. Keeping your pet at the ideal weight for their body can help you avoid extra vet bills for joint problems, exercise programs and special diets, heart problems and more. Just like it is unhealthy for you to be overweight, it is unhealthy for your pets to be overweight too.

3. Do your own exams. I don't mean avoid taking your pets to the vet. What I mean is pay attention to your dog on a weekly basis. Feel his body for lumps, bumps or other issues that aren't normally there. If you perform weekly exams at home, you have a better chance of catching diseases and ailments early on, which may save your pet's life. Catching problems early can also save you money.

The healthier your pet is the less you have to take them to the vet (except for annual check-ups, shots, etc.). By taking these three steps, you can help ensure that you keep the money in your wallet instead of having to shell it out to your vet. All pets have expenses involved in taking care of them, but you can eliminate the unnecessary ones with these three easy steps.

Tuesday, June 30, 2009

3 Ways to Save on Your Vet Bill

Thursday, June 25, 2009

Identity Theft Chat

Millions of Americans each year fall victim to the identity theft thieves. I too was once a victim of identity theft. In my personal situation, it was someone I knew who stole my identity, but it didn't make my nightmare any easier. Not only can identity theft be a hassle for you, but it can wreak havoc on your credit.

I recently came across a new website called Identity Theft Chat. It covers real life stories of identity theft victims so you can learn from the experiences of others how to avoid becoming a victim or how to deal with it if you do fall prey. My story will be featured on the site in the near future but I urge you to take a moment to visit the site to learn how NOT to become a victim.

Wednesday, June 24, 2009

How the Interest on Your Credit Card is Calculated

You certainly know how to use your credit card, but it's also important that you understand how the interest is calculated on the credit card balance you keep on your card. The calculation your credit card issuer uses to calculate the interest on your credit card can vary, but the most popular calculation is compounded interest based on a daily rate.

What in the world does this mean and how does this work?

Let's take a look.

How to calculate compound interest

A typical credit card statement covers a 30 day period (give or take a day or so). If you carry a balance over from the previous month to the new month, then the interest typically starts to accrue on the first day of your new statement period. So if your new statement starts over again today, June 23 and covers purchases made from today through July 22, then the $100 balance you carried over from last month starts to accrue interest from the date of purchase until you pay it off.

Using a compound interest calculation, your card issuer uses a daily rate to figure out how much interest to charge you, which is determined by dividing the annual rate by the 365 days in the year. You accrue interest on the daily average outstanding balance you've have outstanding throughout the month. So as you make charges during the new monthly period, you begin to accrue interest on the average daily balance you have on your account--if you don't pay the balance off by the due date.

Accrued interest may be nominal when your balances are small but as your balances grow, so does the amount of accrued interest. This is when it seems to spiral out of control, causing many consumers to start drowning in a sea of debt. Credit cards may be a big part of your life, but it's important to understand how your credit card issuer is charging you to use the card they've issued to you. It's the only to determine how much that purchase is really costing you.

Tuesday, June 23, 2009

Learn How to Be a Smart Entrepreneur That Survives a Recession

There is no doubt that times right now are tough. As a small business owner, you may be watching as your customers freak out over the headlines hitting the news everyday. Their freak out means they are saving their pennies and may not be spending their money on your products or services. Learn the five steps you can take to survive this recession and any future ones that (hopefully do not) come your way.

5 Ways to Bring Your Small Business Out of the Rubble

1. Be proactive. As a smart business owner, you don't just open your business everyday and hope that customers find you. If you do, then you're in trouble. A successful entrepreneur instead knows who their ideal client is, where to find them and what to say to them when marketing and advertising to them. Then you proactively create marketing campaigns that attract and speak to your ideal clients.

2. They mimic the great ideas of great entrepreneurs. There are great business people all over the world. As a smart business owner, you need to seek out the best business people in the world and see what they're doing. Even if the industry for the business is different from your business, you can find ways to apply their great ideas and actions to your business.

3. Be a leader. The last thing you want to be in the middle of a recession is part of the crowd. During recessions, the middle drops out and you either drown at the bottom and die or move to the front of the line. You want to take a look around and see what the average business owner is doing and then do the direct opposite. The "average" companies sink and drown in a recession and you want to go to the front of the line. For example, many businesses cut back their marketing budget during hard times. The opposite is actually true. Companies should be ramping up on marketing during hard times so your customers will remember your business during great times too!

4. Figure out and use your USP. Your USP is your company's unique selling proposition. Simply stated, it's why your customers should be buying from you rather than somebody else. It may take you some time to come up with your USP, but once you have it figured out, use it to your advantage. It's a surefire way to gain your portion of the business that is out there to be had.

5. The power of attraction and association. Surround yourself with positive thinking business owners and individuals rather than those whining about how horrible life is. When you surround yourself with successful and positive people you'll attract wealth and positivity to your life and your business.

Take these five steps and watch as your competitors close their doors in failure while you emerge as a leader.

Thursday, June 18, 2009

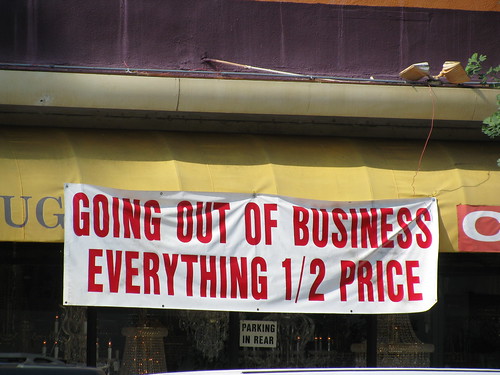

Do Going-out-of-Business Sales Really Save You Money?

There is no doubt that this troubled economy has forced large and small retailers into closing their doors. In an effort to get rid of the merchandise on store shelves, many of these businesses resort to liquidation sales. The more they sell, the less of a loss they walk away with, but what does it mean for consumers buying the merchandise?

Comparison shop

Consumers may think that a liquidation sale means rock bottom prices for them to buy the merchandise they want. In reality though, just because a business is having a liquidation sale does not guarantee its sale price is the lowest. Compare the price of the item at the liquidation sale to at least two other retailers before making a purchase. Comparison shopping is just as important when dealing with liquidation sales as it is with any other major purchase you make.

No guaranteeIt's also important to remember that when you buy an item at a liquidation sale, the store isn't going to be there to stand behind the sale tomorrow. Most liquidation sales are final so if you take your item home and it breaks two days later, you can't exchange it for a new one or get a refund from the store. You'll probably have some protection from the manufacturer's warranty but not from the store itself.

Can going-out-of-business sales save you money? Yes and no. You should comparison shop before making any purchases, including liquidation sale purchases. Plus the safety and security of the retailer standing behind their sale is gone, so you may save a few bucks upfront that turns into a headache if you have to deal with the manufacturer directly if an item breaks, etc., after you've purchase it.

Wednesday, June 17, 2009

What the 2010 Credit Reform Means for Small Business

Small businesses are a special entity. These businesses do not have the funds that big businesses have access to, but still require money to operate on a daily basis. Since small business owners tend to separate their personal finances from those of their business, many bridge the time gap between when they have to pay for business expenses and when they receive customer payments by using small business credit cards.

As part of his effort to combat the financial woes of the nation, President Obama enacted a credit card reform bill in an order to protect consumers from changes to the terms and conditions by the credit card issuers. The bill, which goes into effect in 2010, protects consumers from having their credit card accounts closed—even if their accounts are in good standing—or from interest rate hikes without ample notice. It requires credit card issuers to notify cardholders of interest rate changes 30-days prior, account closures 45-days prior and to send bills at least 21 days prior to the due date. As a credit cardholder, you may sigh in relief because some of the conditions stated in the bill will benefit you in the long.

If you’re the proud owner of a small business credit card, however, don’t sigh too fast. The bill does not extend to protecting small business credit cardholders.

So what does the credit card reform mean for small business credit cards?

Account closures

Credit card issuers of small business cards will continue to have the right to close a small business account without the same amount of notice as consumer cards. This is true even if you have been a model small business cardholder. So if you rely on your credit card to cover small business expenses, your access to this money can disappear in a matter of days. This greatly handicaps small businesses because the owners may no longer have the capital to keep their business doors open. This adds to the number of businesses already having to close because of the bad economy.

Interest rate hikes

Small business credit card exclusion from the reform means interest rates can be increased at any time and without enough notification for the business owner to make other arrangements. These rate hikes can mean the difference between being able to afford making the monthly payment and not being able to afford it. Again, if the line of credit for a small business is cut off because of unfavorable terms, then it may be the demise of the business.

Terms and conditions changes

While the reform protects consumer cards against terms and conditions changes that can adversely affect the cardholder, small business card issuers can continue to change conditions at will. This may mean that small business cardholders receive notice that the issuer is closing their account only a few days before the closure or before a rate increase is instituted. While the reform bill also prohibits card issuers from increasing rates during the first year, this does not apply to business cards.

With millions of small businesses across the nation contributing to the American economy, how is it going to resolve the economic turmoil if these businesses have to close because of unfavorable credit terms and conditions? In short, the new credit card reform does not protect small business credit cardholders. It leaves these cardholders vulnerable to the credit card issuers or forces them to use their personal credit cards to cover business expenses. In essence, it may change the way small businesses do business and have an effect on whether or not they can do business at all.

Tuesday, June 16, 2009

3 Credit Mistakes Married Women Make

Even women who were financially savvy when they were swinging singles turn their backs on their finances once they become blissfully married. This approach to the financial aspect of life is wrong on many levels. With credit scores and credit history playing a starring role in almost everything financial—buying a house, getting a job, obtaining a credit card, and receiving favorable interest rates and terms—it’s important that women do not allow the transition from the single life to a married one to invoke a laissez faire attitude.

Here are the number one credit mistakes married women make and why you should avoid making them.

Mistake #1 Combining all assets and debts

Marriage involves turning two lives into one. Women apparently take this literally. Once the marriage certificate is signed they join all of their assets and debts with their husband. While it is important that husbands and wives are aware of and have a list of all bank, brokerage, credit and debt accounts, it’s also important to keep some of these accounts in your individual names.

The Why

Happy marriages can turn bad and spouses can pass away. When and if this happens it’s important that you have the ability to support yourself. This includes obtaining new credit, renting a home or buying a car. If you relinquish all of your debt and assets to a joint status or in your husband’s name (solely) then any debts or assets established during your marriage may not show on your credit. Lack of credit history or a low credit score can prohibit you from being able to support yourself.

Mistake #2 Not taking joint title of assets

It is important that your name appears on the title to property purchased during your marriage. This mistake occurs most often when titling a home, car, bank account or brokerage accounts. If assets have to be split because of divorce or death your claim to the assets may be challenged. For example, if the home is titled in your husband’s name only--even if you’re the one making the mortgage payments--you are not legally an owner of the home.

The Why

If you’re not showing on title as one of the owners of a piece of property you may not be able to claim ownership even in a court of law. Asset disputes of this nature are determined by state laws, but you can avoid the hassle of proving or requesting ownership by making sure your name appears on title to all of the assets and property you acquire during your marriage.

Mistake #3 Not Reviewing Financial Statements and Bills

The old adage, “What you don’t know can’t hurt you,” should not apply to your financial situation. Married women seem to be the culprit of this action by turning over all financial responsibility to their husbands. The husband reviews the bills and statements, pays the bills and manages the household finances while the wife has no idea what is going on.

The Why

You always need to be in the know of your financial situation. This includes how much money is in each of your bank and brokerage accounts and what debts and assets you have. If your husband has poor money management skills and is running your finances into the ground you need to catch this before it causes a credit problem. Late payments and not making payments on time can cause your credit score to plummet, which can damage your ability to obtain new credit in the future.

Women need to be financially savvy even after marriage in order to maintain a good credit score and history, which plays a major role in everything financial. It’s important that women do not relinquish financial responsibilities to their husbands, but rather are involved and engaged in the household finances.

Thursday, June 11, 2009

Free Money

You've seen them--the commercials where the Publishers Clearing House shows up with the giant size check and gaggle of balloons to announce to the person behind the door that they're a content winner! Who doesn't love to win free stuff, especially when that free stuff is money. Well, you've got to play it to win it so find out the secrets behind being a sweepstakes winner.

1. You have to enter to win, so head on over to www.Sweepsadvantage.com and www.Online-sweepstakes.com and check out some of the sweepstakes available. Companies, blogs and websites run contests all the time. Enter as many contests and as often as you can. It's the only way you have a chance to win. Sometimes the prizes are items, trips or stays in hotels, but other times it's cold hard cash.

2. Save time with an auto-fill program. If you don't have a form auto-filler, you can download one for free online. This cuts down on the time it takes you to enter all of your information in contest forms and gets you closer to the time when your name is picked as the winner.

3. Persistence is the key. Like almost anything, you have to keep trying over and over again until you get it right. Since contests tend to have a long lead time, it can take six months to a year to see the fruits of your labor, so be persistent. Set some time aside for your entering contests or at least regularly enter the contests you come across. The more contests you enter the better your chances of winning free stuff.

Tuesday, June 9, 2009

15 Ways to Save Money (and Energy) at Home

Whether it's the troubled economy or you're trying to get your finances in order there are steps you can take at home to cut back on your expenses. As an added bonus these are also ways you can save energy, so you're saving your money and the environment simultaneously. Implement some of these suggestions and you can add a couple thousand dollars to your bank account.

1. Put outdoor lights on a timer or use sensors. This keeps lights from staying or coming on during the daylight hours.

2. Have a conversation with your utility company. Utility companies across the country are offering rebates and incentives to customers that take conservation measures. It may be a rebate for using compact fluorescent light bulbs or for installing energy efficient appliances. It doesn't hurt to ask, so check out the website or give the power company a call.

3. Green your holiday lights. Use LED light strings during the holidays. It's shown to save you in the neighborhood of $11 per season.

4. Let the dishwasher wash the dishes. Consumer Reports found it's unnecessary to rinse your dishes before you load them in the dishwasher. You can save up to 6,500 gallons of water each year by letting the dishwasher do its job.

5. Let the washing machine work. Speaking of washing--let your washing machine and detergent do its job with the cold cycle. Most detergents have germ killing agents so hot water isn't necessary to clean the germs. Cold water does the trick!

6. Line dry clothes. When possible, dry your clothes on a clothes line or hang your clothes on hangars and hang them inside the house. If you have to use the clothes dryer, don't put too many clothes in each cycle.

7. Lower the temperature two degrees. When nobody is home or right before you welcome guests, lower the temperature on the thermostat a couple of degrees in winter. This helps to keep the heater from kicking on as often--saving you money and saving energy.

8. Insulate and seal. Reduce the cost of energy by about 30 percent by insulating and sealing cracks in ducts.

9. Insulate properly. Make sure your home is properly insulated. This is especially true for older homes. Proper insulation can cut your heating and cooling bills down by 10 percent.

10. Call in a professional. Professional energy auditors can inspect your home, using professional equipment, to find energy leaks. You can find a professional energy auditor in your area at www.resnet.us.

11. Clean the fridge coils. By keeping the coils under or behind the fridge it helps the fridge to run more efficiently, which saves energy and money.

12. Use power strips. Plug items into a power strip that can be turned off all at once. Turn the strip off when these items are not in use.

13. Portable heating and cooling units. Instead of running the central heat or air system, use portable heating and cooling systems to heat and cool the areas of your home where needed.

14. Block out the sun. Use shades, drapes and curtains to block out the sun on hot days. This helps to keep the air conditioner from kicking on more because the sun streaming in the windows is raising the temperature of the room.

15. Use trees for shade. Plant shade trees on the west side of your home to help shelter it from direct sun and keep the inside temperature cooler.

Thursday, June 4, 2009

Paying Off a Mortgage isn't Always the Way to Go

There are two schools of thought when it comes to paying off a mortgage. The first school of thought thinks that the faster you pay off your mortgage, the less you pay and you get rid of the debt. The second school of thought believes your money is better spent elsewhere--make the monthly mortgage payment, take your tax write-off and use the "extra" money to invest in something that brings you a greater return than the after-tax interest rate you're paying on your mortgage.

Which thought process is better? Both have benefits, but put your personal opinions aside for a moment and ask yourself the following questions.

1. Realistically, how long am I going to live in or own this home?

2. How much mortgage interest are you writing off on your taxes?

3. What investment options are available to earn a higher rate of return than what you're paying on an after-tax basis on your mortgage?

Now, let's tackle the answers to these questions one at a time.

1. The national average for Americans to live in or own a home is five to seven years. After the five or seven years, sometimes in less than five years, we move, we well the home, we buy a new home or return to renting.

Now, if you take a look at the amortization schedule on a 15 or 30 year mortgage, for example, you are paying mostly interest for the first half of your mortgage, which works since we are only living in them for five to seven years anyway. It's like renting with a tax deduction!

2. The ability to deduct the mortgage interest from your taxes varies from situation to situation, so you need to speak with your tax advisor about your own personal write-off. Generally speaking, the entire interest portion of mortgage on a primary residence is fully tax deductible. This may be one of your biggest tax deductions. It some cases, it may be one of your only tax deductions, so why would you want to get rid of it?

3. In today's economy you may be hard pressed to find an investment that brings you a greater rate of return than the after-tax rate of your mortgage. This isn't and won't always be the case, however. And it's important to remember that once you sink your money into the home it is gone until you sell the home or tap into the equity of the home with an equity line or loan.

What if there is an emergency? What if you can turn a profit by buying a new piece of real estate and renting it out? What if you can invest your money in a mutual fund that brings you a greater return than you're paying out on your mortgage?

If you've already spent your money paying down your mortgage, then the opportunity for you is gone unless you want to pay a lender to allow you to tap into the equity.

These concepts don't apply to everyone. This is not a one-size-fits-all solution, but a mortgage is seen as a good debt because of all of the benefits associated with it. A credit card, however, is considered a bad debt (not tax deductible and extremely high interest rates). If you want to use your money to pay something off, get rid of your bad debt instead and leave your good debt working for you.

Tuesday, June 2, 2009

Is Staging Your Home the Answer to Selling it?

You make a house your home with all of the personal items and touches you add to it. What makes a house a home for you may be completely different for the potential buyers you're trying to sell your home to. Good real estate agents tell their clients how to prepare their home for sale by cleaning it, moving furniture a certain way and anything else that makes the home look more welcoming.

The bottom line is potential buyers need to be able to visualize themselves living in your home with their own things, not yours. Do you need a professional house stager to help you accomplish this? In a buyer's market with so much competition, it can't hurt. Whatever you decide, here are some ways you can prepare your home for a faster and easier sale.

3 steps to prepare your home for sale

1. Neutralize

Home staging is not about the style you decorate your home. It's more about the depersonalization or neutralizing of your home. Some of these things you can do yourself such as removing family photos, personal decorations, books and magazines.

2. Clean

The cleaning portion of the staging process applies to the inside and outside areas of the home. It may include cleaning out gutters, mowing, weed eating, landscaping and a new coat of paint to the front door. It's also about neutralizing the area for personal items such as garden doodads, wind chimes and relocating your RV from the driveway. Once the outside looks appealing enough to attract buyers, it's time to move on to the inside.

Scrubbing your house from top to bottom and being conscious of everything from odors to how clean the grout between the tile is can make or break the first impression of the potential buyer. It may be worth the expense to hire a professional cleaning service to give the home a good once over that you can upkeep in the process.

3. De-clutter

In conjunction with the cleaning, it's also recommended that sellers pack away the majority of their belongings and remove them from the home or store them in the garage. Removing up to two-thirds of your belongings from the home helps to de-clutter it and puts you one step ahead in the moving process. Some of the first items you should pack are personal photos, knickknacks, collectibles, books, magazines, blankets and throw pillows. Remove as much from the kitchen counters as possible, storing small appliances away in cabinets, selling or donating items you no longer need.

You're preparing your home like a matchmaker prepares two people for a date. Take a good hard look at the benefits of your home. What are its best features? Find ways to arrange furniture, place lighting or accentuate these benefits. Remember that less is more so the less furniture, area rugs and decorations you have the better.

Turn to the professionals

Whether you're not able to stage your home on your own or you've been trying to sell your home and it isn't working, a professional home stager may be the answer. A neutral third party may be what's needed to make the right first impression, especially since you don't get a second chance to do so with potential buyers. To find a professional home stager in your area, visit the International Association of Home Staging Professionals website at www.iahsp.com.